The Market Was Finally Waking Up. Then the World Got Complicated.

I've been doing this long enough to know that the housing market doesn't move on a straight line. Rates drop, buyers come back, something unexpected happens, and suddenly everyone is waiting again. That's exactly what played out in the first months of 2026, and it's worth walking through, because what it means for buyers right now is more significant than most people realize.

A Market That Had Been Stuck for Years

To understand where we are, you need to appreciate how deep the slowdown went. The U.S. housing market closed out 2025 with roughly 4.06 million existing home sales for the year, well below the historical average of about 5.2 million annual transactions. That was the worst year for sales in three decades. Mortgage rates had been hovering in the 6% to 7% range throughout 2025, keeping millions of would-be buyers on the sidelines and keeping would-be sellers locked in place, unwilling to trade their 3% pandemic-era mortgages for anything close to today's rates.

The result was a market in suspended animation. Demand was real. The housing shortage was real. But affordability was stretched thin enough that activity ground to a near-halt. Most buyers and sellers were simply waiting.

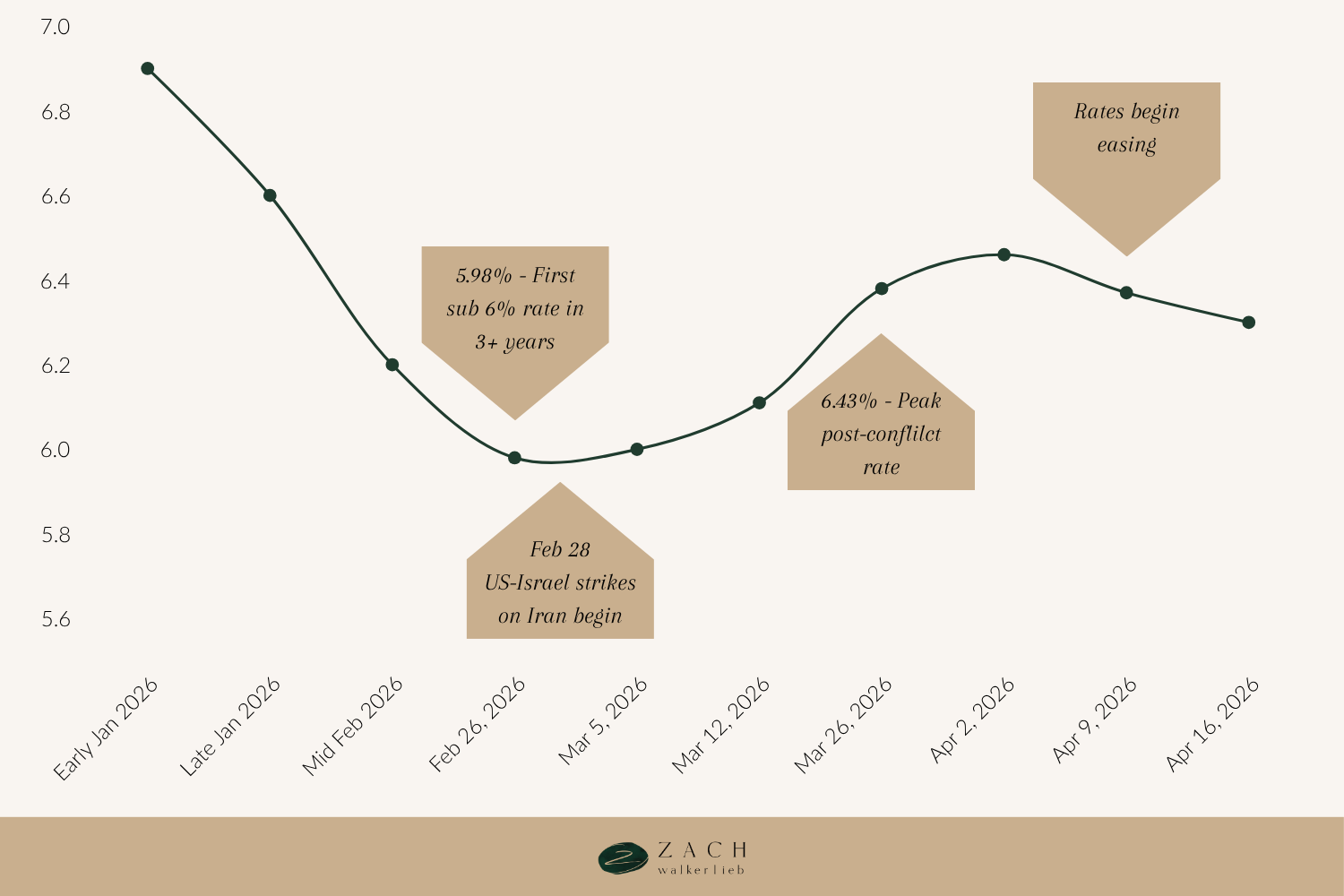

Early 2026 Looked Like the Turning Point

Heading into this year, there were genuine reasons for optimism. Mortgage rates were drifting lower through late 2025 and into early 2026, and in late February, the 30-year fixed mortgage dipped to 5.98%, the first time it had fallen below 6% in more than three years. That number matters more than it might seem. There's a psychological threshold around 6% that changes how buyers think about their monthly payment. When we crossed it, the phone started ringing differently.

Listings that had been sitting started moving. Buyers who had been waiting on the sidelines began re-engaging, particularly at higher price points where rate sensitivity is often lower. Properties above $1 million were seeing real interest and, in some cases, multiple offers. The spring selling season was setting up to be the most active in years.

Then Geopolitical Risk Hit

In late February, the U.S. and Israel launched joint strikes on Iran. What happened next in the financial markets was almost immediate. Oil prices surged. Inflation fears returned. Investors sold bonds, which pushed Treasury yields higher, and since mortgage rates track the 10-year Treasury yield, rates followed right behind.

Within weeks, the 30-year fixed mortgage had climbed from 5.98% back into the mid-6% range, settling around 6.3% to 6.5%. The improvement in affordability that buyers had spent months waiting for was effectively erased. Mortgage applications dropped sharply. Purchase activity stalled. The buying momentum that had been quietly building simply stopped.

None of that should be surprising. Real estate decisions involve large long-term commitments. When geopolitical events increase economic uncertainty, buyers pause, even when the underlying fundamentals are still solid. It's not irrational, it's just how confidence works.

Where Things Stand Right Now

The picture is more nuanced today. As the conflict has shown signs of stabilizing, mortgage rates have begun drifting slightly lower, and buyer confidence has started to return. Properties are again receiving strong interest across multiple price points. Demand never disappeared, it paused.

Here's what hasn't changed through any of this: the structural housing shortage. The U.S. is short roughly 4 million homes, the result of more than a decade of underbuilding that no single year of new construction can fix. That supply deficit doesn't care about geopolitical events. When buyer confidence comes back at scale, and it will, the underlying imbalance between supply and demand will push prices higher again.

Right now, buyers have something rare: time and leverage. They can still negotiate on price, terms, and concessions in ways that were nearly impossible during the pandemic housing boom. Sellers are more patient than they were two years ago, which means deals that simply weren't available then are on the table now.

That window may not stay open long. Once rates stabilize and economic confidence improves, the pent-up demand built up over three years of suppressed sales will likely surge back into the market, exposing the same supply constraints that have defined housing for the past decade. The next 6 to 12 months may represent one of the better buying opportunities we've seen in years, not because conditions are perfect, but because competition hasn't caught up to demand yet.

Market data tells part of the story. The rest depends on your neighborhood, your timeline, and your goals. I'm happy to help you put it together.

About Zach WalkerLieb

Zach WalkerLieb is a top Las Vegas real estate agent and Managing Partner of Willow Manor, one of the city's leading luxury real estate teams. With hundreds of millions in closed sales, Zach brings a deep, practical understanding of the Las Vegas housing market, from high-end luxury to the everyday realities shaping neighborhoods across the valley. Beyond real estate, he serves as Chairman of the Board for Habitat for Humanity Las Vegas and as a board member of Keystone Corporation, giving him firsthand insight into housing policy, affordability, and long-term community development. Known for clear thinking, market honesty, and local expertise, Zach writes to help buyers, sellers, and investors make confident, well-informed decisions in Las Vegas real estate.